Mobile App Ad Spend: Who’s Getting the Lion’s Share?

GamechangerSF recently published data about the top global media channels for mobile app ad spend, quality, and scale. At Braavo, we fund user acquisition and growth for mobile apps and games – which means we have a unique view into what founders and developers are spending on.

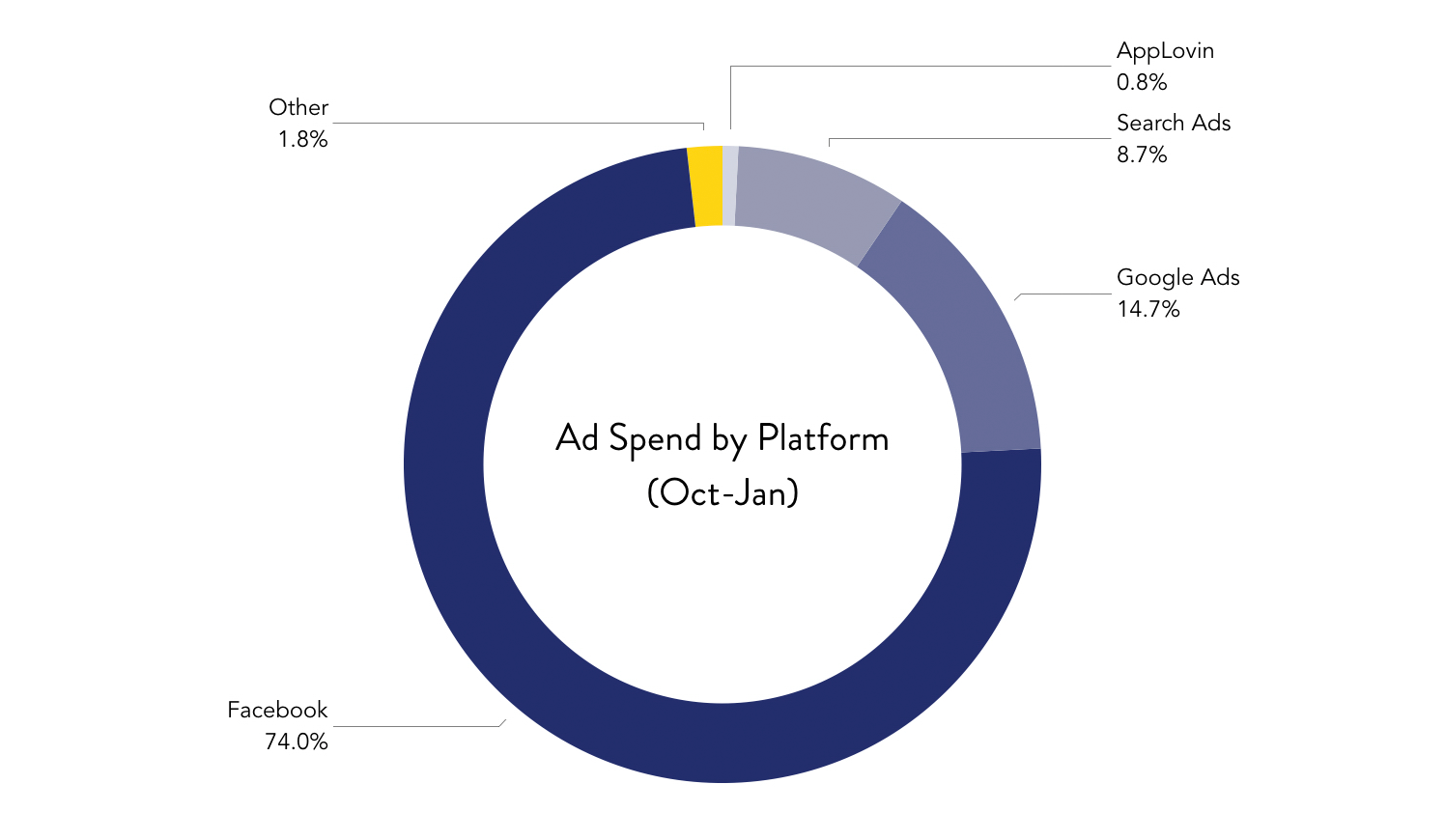

We decided to analyze our own data from the past 3 months to determine in which channels our users have been investing. For this data set, we analyzed tens of millions in ad spend, but excluded major industry leaders to provide more relevant data for our audience.

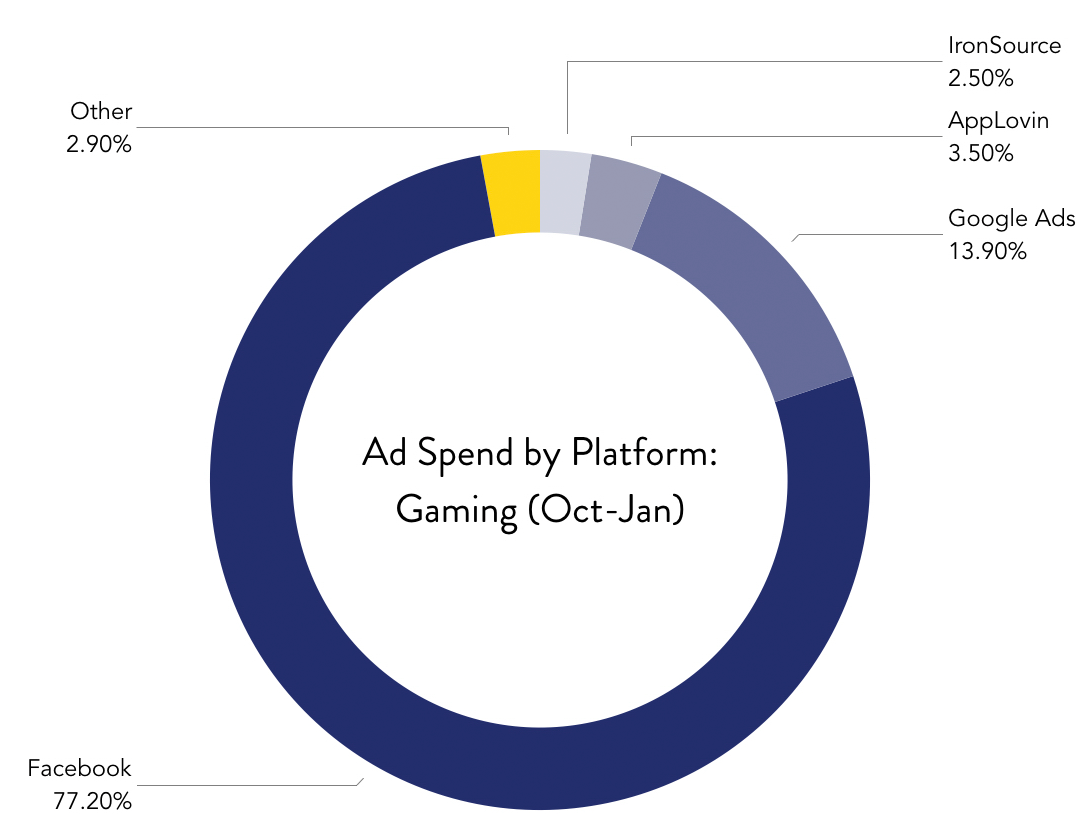

Mobile App Ad Spend by Platform – Gaming

Across the board, we found that Facebook takes up the majority of ad spend across both of our gaming and non-gaming portfolios. Somewhat surprisingly, for gaming apps, Facebook had a disproportionate share of the market. We’ll delve into that a little further below.

Facebook drove almost 80% of spend, with the remaining 20% split between Google Ads, ironSource, AppLovin and a handful of other gaming-specific ad networks. As we hinted earlier, for the gaming segment of our portfolio we would have expected a broader distribution across platforms like Applovin, IronSource, Vungle, Unity et al. As it turns out, unless you’re spending millions per month on marketing your game, it probably makes sense to allocate the majority of your time, energy and resources on Facebook (and to a lesser extent Google) until you exhaust the audiences on those channels.

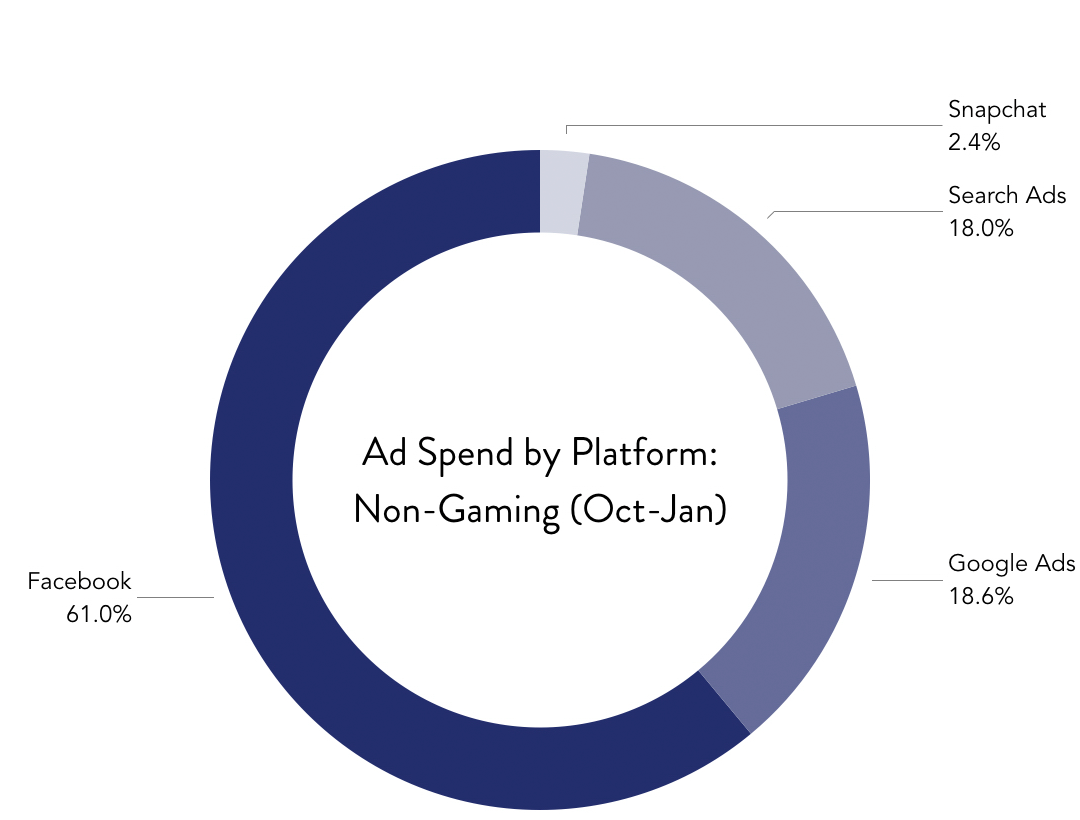

Mobile App Ad Spend by Platform – Subscription/Non-Gaming

For our general/subscription portfolio, Facebook is still a major driver of growth. However, other channels took up a greater proportion of ad spend compared with games:

Facebook drove about 60% of ad spend, Google Ads and Search ads accounted for about 37%, and a small percentage went to Snapchat.

Analysis and Conclusions

In general, we found that most gaming apps (outside of the market leaders) are continuing to invest heavily in Facebook. Non-gaming apps, health and fitness or entertainment apps, play a similar but somewhat different game, distributing spend somewhat more evenly across other channels, including newer platforms like Snapchat.

We’ll be curious to see if and how players like TikTok become a part of the media landscape in the coming months. We’ll also be curious to see if ad spend for gaming apps begins to resemble subscription apps if gaming subscription models become more established.

Related posts

Why Consumer App Founders Should Be Prepared For Q5

Every app founder knows Q4. You brace for CPMs to spike, you fight the algorithm against every other DTC brand trying to cash in on multiple major holidays, and your…

Building an app? Here are the app finance trends shaping the industry in 2026

In 2026, running an app looks more like a cash flow exercise than building a brand. The strongest app businesses today are not just good at monetization, they are good…

Why Your App Marketing Strategy Should Include a Web2App Funnel

Eugene Strelets is a mobile growth and product manager with over four years of experience in data-driven experimentation. With a deep focus on driving mobile products to the next level…